The Company

Applied Optoelectronics designs, manufactures and sells fiber‑optic components and transceivers used in data communications, cable TV systems, fiber‑to‑the‑home and telecommunications networks.

Financials

Bull Case

- With the build out of AI clusters, there is a need for GPUs to exchange data at very high rates. Network bandwidth, not compute is becoming the bottleneck. AAOI makes the critical optical transceivers enabling 800G, 1.6T data rates needed by modern data centers.

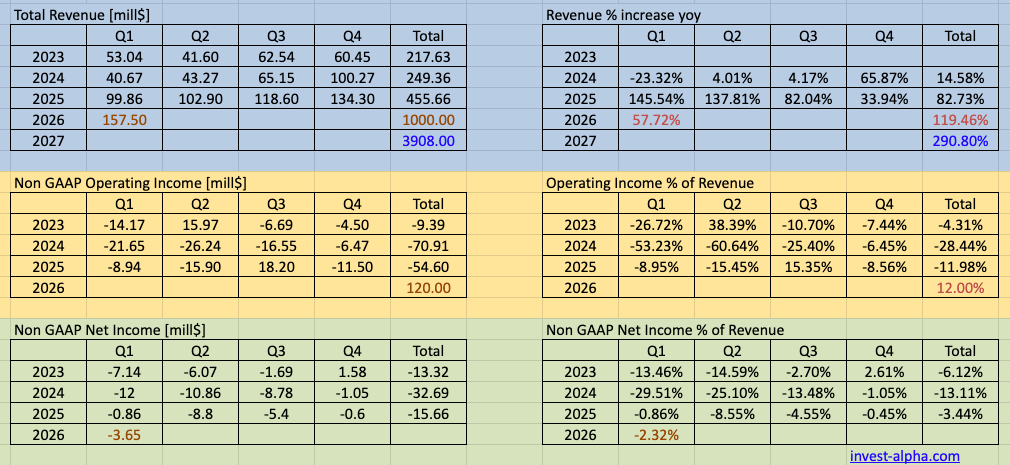

- Management is forecasting growth 120% growth in 2026 and 290% growth in 2027. From management statements these numbers are supply constrained, the actual demand is even greater.

- Market is undergoing a transition from 400G to 800G and is an opportunity for companies like AAOI to grab market share from dominant Chinese players like Innolight.

- AAOI counts 4 of the hyperscalers as customers with a new one expressing interest for it’s 800G products as recent as Q4 2025.

- Management believes demand for 800G products is exceeding their supply capability and is expanding manufacturing.

- AAOI has manufacturing capability within the US at their Texas facility. Given the Manufacture in US emphasis of the administration this might prove to be an advantage.

Bear Case

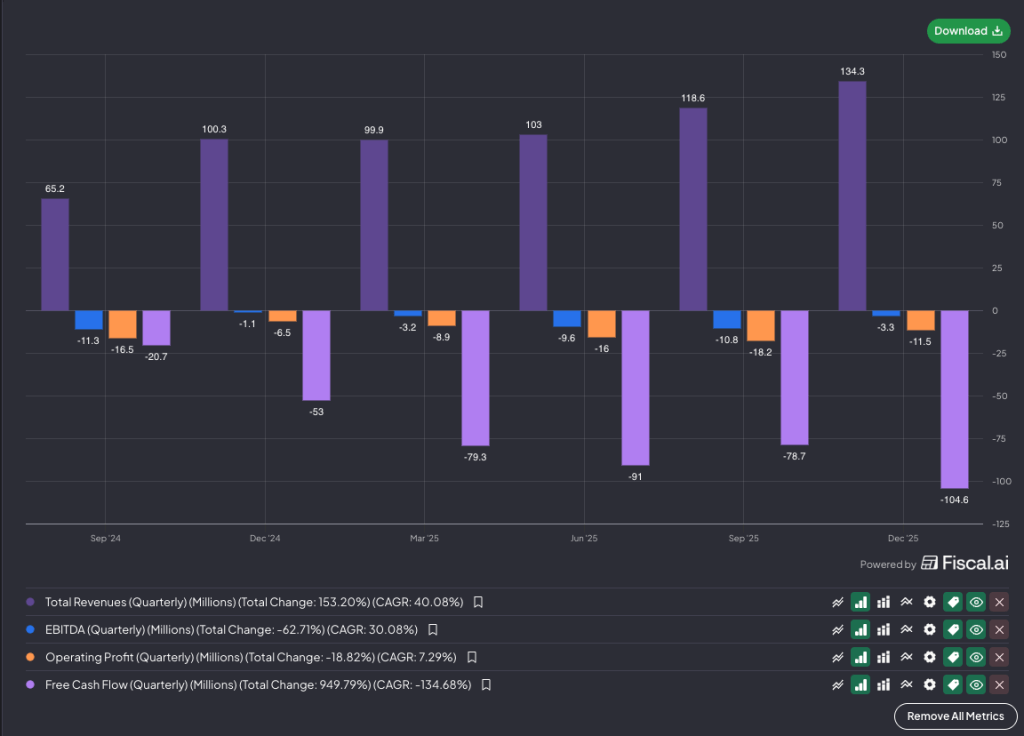

- Free Cash Flow is increasingly negative as each quarter goes by. Company is spending on expanding manufacturing to meet demand.

- Demand pull forward as this AI data center build out accelerates. Any pullback in capex by the Hyperscalers will cause a massive rerate of this name.

Management Outlook

- During the quarter, we announced that we received our fourth 800G volume order from one of our major hyperscale customers to support its AI data center growth. We continue to work with this customer to finalize the firmware used in this module to ensure interoperability across their network, which we believe will be completed in March.

- We have begun ramping our production of this 800G module in anticipation of a strong volume ramp starting in Q2. 800G is expected to dominate our revenue beginning in Q2.

- Forecast demand for 800G modules are projected to exceed our production capacities to mid-2027, and we are working to add additional capacity to meet this demand.

- we have had indications from another existing hyperscale customer that they intend to begin to order 800G from us soon.

- a new hyperscale customer has begun discussion about qualifying our 800G and 1.6T product just within the last few weeks.

- Looking more broadly at 2026, while it is still early in the year, we expect to generate over $1,000,000,000 in revenue this year, with a non-GAAP operating profit of over $120,000,000. This revenue level is limited by our production capacity and supply chain, not market demand, which we believe is much larger.

- By the end of this year, we will be capable of producing over 500,000 pieces of 800G and 1.6 terabit products per month

- We have recently had dialogue with another large hyperscale customer who has been a long-term customer of ours, and who is eager to begin qualification efforts for our 1.6 terabit products. This customer has also indicated a desire to purchase potentially significant quantities of 800G products from us in 2026 and 2027. We continue to discuss capacity availability and expect orders for 800G from this customer soon. It is also important to note our 800G and 1.6 terabit products can be manufactured on the same production line with the same process.

- We believe that in the future, CPO will continue to drive increased demand for high power lasers, and we plan to continue to expand our laser manufacturing capacity in Texas in order to accommodate these future growth drivers.

- Given the recent surge in customer inquiries and apparent rising demand, we believe that by mid-2027, 100G and 400G revenue will be approximately $90,000,000 monthly, 800G revenue will be approximately $217,000,000 monthly, and 1.6 terabit revenue will be approximately $71,000,000 monthly. Altogether, this represents $378,000,000 in monthly revenue for transceiver products. —it is limited by our capacity and the supply chain. It is not limited by the customer demand.

- there is a huge issue of laser shortage. And, actually, even some supplier to us want to get this from them. We—we had at least one year, even longer. So that is why we announced we will invest $300,000,000 in Texas—triple, even more than triple. The purpose, as we said, we need to increase our laser capacity by Q2 next year, and that is to fulfill our transceiver demand.

- let me say that more than one customer, at least two or even three, they would like to buy all the transceiver we can make for 800G and 1.6. Because Applied Optoelectronics, Inc. laser. And right now, it is limited by our capacity and the manpower and the supply chain. So that is why we are trying everything to ramp up. It takes time. It takes time. That is why I say going on this year, we say $1,000,000,000. And let me say that dimension is much, much bigger than $1,000,000,000. But that is a number we feel comfortable. At least we feel minimum 99% confident we can deliver.

TAM / CAGR

The global fiber‑optic transceiver market is currently estimated at $10 billion+, with forecasts predicting a CAGR of ~8–10% over the next several years, driven by AI infrastructure build‑out, hyperscale data centers, and shifts to higher‑speed optics

Products

1. Datacenter Optical Transceivers (Primary Business)

| Product | Description | Competitors | Revenue % | Growth |

|---|---|---|---|---|

| 100G Transceivers | Legacy hyperscaler optics | Innolight, Eoptolink, LITE | ~5–10% | Declining |

| 400G Transceivers | Current deployed base | Innolight, COHR, LITE | ~10–15% | Flat to modest |

| 800G Transceivers | AI cluster backbone | Innolight, COHR, LITE | ~50–60% (rapidly growing) | Explosive |

| 1.6T Transceivers | Next-gen AI optics | COHR, LITE, AVGO (CPO alt) | ~0–5% (today) | Future ramp |

2. AOC (Active Optical Cables)

| Product | Description | Competitors | Revenue % | Notes |

|---|---|---|---|---|

| AOC Cables | Fiber + integrated optics in cable form | Innolight, Amphenol, AECs from CRDO, ALAB | ~5–10% | Simpler deployment vs pluggables |

3. CATV Broadband Products (Legacy but Still Meaningful)

| Product | Description | Competitors | Revenue % | Growth |

|---|---|---|---|---|

| CATV Optical Transmitters | Headend equipment for cable networks | CommScope, Harmonic | ~15–20% | Low growth |

| CATV Optical Receivers | Signal distribution in cable infra | Same | Included above | Stable |

4. Optical Components (Mostly Internal)

| Product | Description | Competitors | Revenue % | Notes |

|---|---|---|---|---|

| Lasers (DFB / EML) | Light source for transceivers | LITE, COHR | Minimal external | Mostly internal use |

| Photodiodes / Receivers | Signal detection | COHR | Minimal | Vertical integration |

5. Emerging / Upcoming Products (Very Important)

A. 1.6T Transceivers

| Feature | Details |

|---|---|

| Speed | 1.6T |

| Timeline | 2026–2027 ramp |

| Competitors | COHR, LITE |

| Importance | Next AI upgrade cycle |

B. Silicon Photonics-Based Transceivers (Under Development)

| Feature | Details |

|---|---|

| Goal | Lower cost + power |

| Competitors | Intel, Broadcom |

| Status | Early / evolving |

Business Model

AAOI builds optical transceivers, subassemblies (light engines), and packaged solutions using in-house laser tech. It sells both B2B to OEMs and directly to cable multiple-system operators under its Quantum Bandwidth™ brand. Revenue scales with volume in data‑centers and cable upgrades; margins benefit from proprietary manufacturing and rising automation.

Customers

Microsoft (Azure) – AAOI has an ongoing multi-year supply relationship with Microsoft. Microsoft has worked with AAOI on designs and product qualifications for optical transceivers and related components; Microsoft accounted for a significant portion of AAOI’s data-center revenue in recent years.

Amazon (AWS) – Reports indicate Amazon has entered into a long-term supply agreement with AAOI that could be worth billions over time, and Amazon is expected to be a major buyer of 400G/800G optical modules and transceivers.

Unnamed Major Hyperscale Customer – AAOI announced that it received its first volume order for 800G transceivers in late 2025 from a “major hyperscale customer” (not publicly named). This customer has also placed significant orders for 400G products, but the company did not explicitly disclose the name in the press release.

Competitors

Top 3 direct competitors in the fiber‑optic transceiver space:

- Lumentum Holdings – offers datacenter and telecom optics

- Ciena – broad portfolio including high-speed transceivers

- Infinera – specialist in packet-optical and transceiver modules

Founding History

Founded in 1997 and headquartered in Sugar Land, Texas, AAOI went public via IPO in March 2014 (raised ~2.7 M shares). Its CEO and founder, Dr. Thompson Lin, has overseen a strategic pivot from cable-optic components to high-speed data-center transceivers with laser integration capabilities