The Company

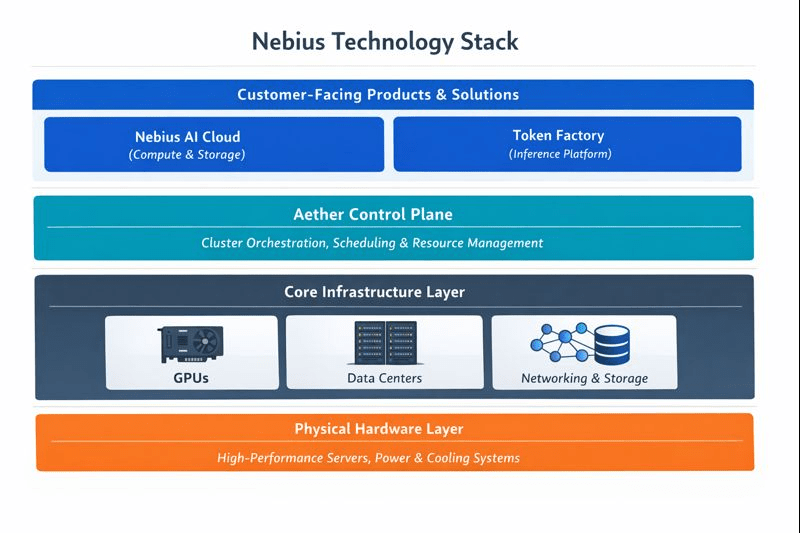

Nebius Group N.V. is a Nasdaq-listed European AI infrastructure company headquartered in Amsterdam. It provides a full-stack GPU‑accelerated cloud platform—offering compute, storage, developer tools, orchestration, and managed services—catering specifically to AI training and inference workloads. It operates flagship subsidiaries including Nebius.AI, Toloka (AI data services), Avride (autonomous driving), and TripleTen (edtech).

Financials

Bull Thesis

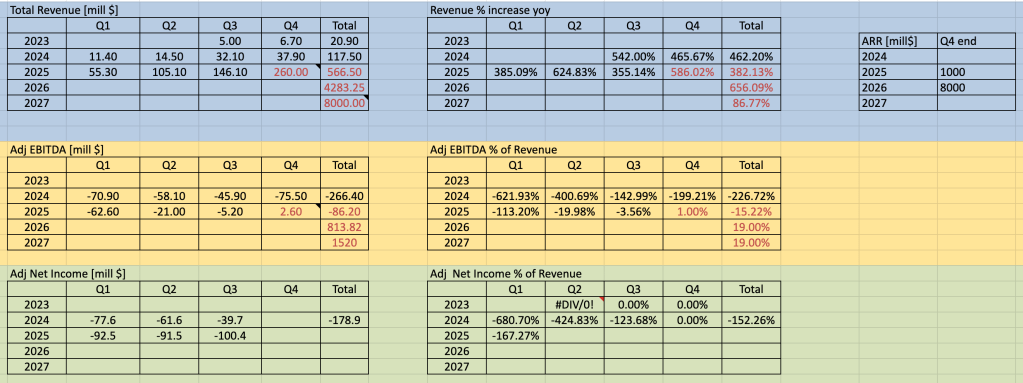

- Management expects Core GPU Compute ARR to grow from 1Bill$ end of 2025 to 8Bill$ end of 2026 at the midpoint. Adj EBITDA is ~19% at the moment and even if this stays steady points to massive growth over next couple of years.

- Massive 18.5 Bill$ contract with Microsoft and a 3 Bill$ contract with Meta over 5 years gives credibility to their product.

- Nebius’ Europe roots is a differentiated advantage from Coreweave, IREN for customers with sovereignty or jurisdiction concerns.

- Nebius offers an inference software platform the Token Factory that differentiates it from other Neoclouds.

- Nebius has a few other promising business segments such as the Avride delivery robots that have seen growing adoption and blue chip partnerships such as with Uber.

Bear Thesis

- Capex risk: Neoclouds are a hedge by the hyperscalers against overinvesting in capex, a wait and see approach to see how AI demand evolves. If AI demand wanes, hyperscalers might not renew contracts and the massive capex buildout will become a liability.

- Pricing pressure risk: As hyperscalers expand GPU offerings and neocloud competition intensifies, Nebius may face price compression or less favorable contract terms (especially if supply loosens).

Management Outlook ( Q3 2025 )

- Revenue :

- we can achieve annualized run rate revenue, ARR, of $7 billion-$9 billion by the end of 2026.

- Contracts :

- Q3 demand was very strong. We sold out all of our available capacity. We continue to see a consistent trend. Every time we bring capacity online, we sell all of it.

- New contract with Meta of 3Bill$ for next 5 years. Demand for this capacity was overwhelming, and the size of the contract was limited to the amount of capacity that we had available, which means that if we had more, we could have sold more.

- Capacity :

- In order to meet the growing demand, we have accelerated our plans to secure more capacity, and this is actually our main focus for now. Capacity today is the main bottleneck to revenue growth, and we are now working to remove this bottleneck. Contracted power expected to reach 2.5GW and connected power 1GW by 2026.

- Long term focus is to build out the AI cloud to serve end customers directly, not just the hyperscalers.

- Products:

- We have a large pipeline of new software and services that we are continuing to build, which will differentiate us from other cloud companies.

Bookings

| Customer | Revenue | Contract term |

|---|---|---|

| Meta | $3 billion — may expand as new capacity is onboarded | Announcement: Nov 11 2025 ( Q3) Term: 5 years |

| Microsoft | $17.4 billion — may expand to ~$19.4B if Microsoft purchases additional capacity. | Announcement: Sept 8, 2025 Term: 5 years Start: end 2025 – end 2030 |

| Israel — National AI Supercomputer | $115mill | start early 2026 |

TAM / CAGR

- TAM for AI infrastructure is projected to reach 3-4 Trill $ by 2030 from the estimated 800 Bill$ spend expected in 2025 according to Nvidia. This is a 35% CAGR.

Nebius Business Segments

| Business Segment / Unit | Short Description | Approx. % of Revenue |

|---|---|---|

| Core AI Infrastructure (Nebius AI Cloud) | Full-stack AI-native GPU cloud offering compute, storage, networking, orchestration (Kubernetes/Slurm), and enterprise tooling for AI training and inference. This is the economic engine of the company. | ~75–80% |

| Token Factory | Production-grade inference and model deployment platform built on Nebius AI Cloud. Focused on scalable, predictable, enterprise inference for open-source and custom models. | ~5–10% |

| Avride | Autonomous driving and robotics business (robotaxis, delivery robots). Operates largely as a venture-style growth unit with partnerships (e.g., ride-hailing, OEMs). | ~5% (or less) |

| Toloka (Equity / Deconsolidated) | Human-in-the-loop data labeling and evaluation platform for AI models. Now primarily an equity stake rather than a consolidated operating segment. | ~5–10% (declining) |

| TripleTen | Edtech / reskilling platform offering bootcamp-style programs in software, data, and cybersecurity. Non-core to AI cloud strategy. | ~3–5% |

| Other Equity Stakes & Incubations (e.g., ClickHouse stake) | Minority investments and strategic holdings in complementary data and infrastructure software companies. | <2% |

Datacenter Locations

| Location | Status | Capacity |

| Mäntsälä, Finland | Operational, with expansion underway | Up to 75 MW |

| Vineland, New Jersey, USA | Planned/Under construction | Up to 300 MW |

| Kansas City, Missouri, USA | Operational (colocation) | Expanding from 5 MW to 40 MW |

| Keflavik, Iceland | Under construction (colocation) | 10 MW cluster |

| Paris, France | Operational (colocation) | 5 MW |

| Longcross Park, Surrey, UK | Upcoming (colocation) | Initial deployment of 4,000 NVIDIA Blackwell Ultra GPUs |

| Tel Aviv, Israel | Planned | Estimated 5 MW (based on first phase of 4,000 GPUs) |

Nebius Technology Stack

Business Model

Nebius operates a consumption-based cloud service for AI workloads, generating revenue per GPU-hour and additional usage metrics. It integrates vertically by designing its own hardware and managing data center infrastructure. Subscriptions to developer tools and managed services add recurring revenue. Its subsidiaries diversify the income mix through data labeling, autonomous tech, and edtech services.

Customers

Competitors

GPU Cloud and AI Services Competitors

- CoreWeave – GPU cloud with bare‑metal focus and rapid deployment of latest Nvidia hardware

- IREN (formerly Iris Energy) – GPU cloud with a notable focus on using renewable energy sources to power its data centers. It also maintains a business in Bitcoin mining, which it has used to acquire the necessary infrastructure and expertise to pivot into the AI cloud space.

- Lambda Labs – Provides GPU servers, cloud instances, and AI model training services.

- TensorWave – AI infrastructure provider specializing in GPU accelerated workloads

Differentiation vs CoreWeave

Where Nebius can be different (positives):

- Geography / sovereignty angle: Nebius has a stronger “Europe-first” narrative (helpful for regulated or sovereignty-sensitive customers).

- Early proof of segment profitability: Nebius highlighting ~19% core infra adj EBITDA margin is a tangible unit-economics datapoint.

Where CoreWeave is often seen stronger (risks for Nebius):

- Scale & training reputation: CoreWeave markets very large-scale GPU clusters and performance/“goodput” style metrics, with strong visibility in frontier-training workloads.

- Partner ecosystem: CoreWeave has publicized major multi-year partnerships (e.g., capacity arrangements with Nvidia / large enterprise deals), which can de-risk utilization in investors’ eyes.

Differentiation vs IREN (Iris Energy)

Different “starting point” business model:

- IREN is power + data-center first, cloud second. It emphasizes secured power capacity and operating data centers (renewable narrative), then layers AI cloud/GPU services on top.

- Nebius is cloud platform first (software + orchestration + customer-facing GPU cloud), with the infrastructure build serving that cloud go-to-market.

Why this matters:

- IREN advantage: power access / site development can be a strategic moat when the bottleneck is MW availability.

- Nebius advantage: developer experience + cloud abstraction can make onboarding easier and improve stickiness versus a more infra-centric provider.

AI Inference Software Platforms

| Platform / Provider | Primary Focus | Deployment Model | Key Strengths | Typical Use Cases |

|---|---|---|---|---|

| Nebius Token Factory | Enterprise inference platform optimized for open models | Hosted / Cloud Native | Cost-efficient scaling, multi-tenant APIs, autoscaling, SLA governance | Production inference, customized models, regulated workloads |

| OpenAI API (ChatGPT / Inference) | Managed model + inference service | Hosted | Best-in-class LLMs, high availability, simple API | Consumer apps, prototypes, enterprise APIs |

| NVIDIA Triton Inference Server | GPU-optimized model server | Self-managed / Cloud | High performance, multi-model support, extensible backends | On-prem, cloud GPUs, research & infra |

| AWS Inferentia / SageMaker Inference / Bedrock | Managed inference + enterprise integrations | Hosted on AWS | Deep AWS ecosystem, security, monitoring | Enterprise AI at cloud scale |

| Google Vertex AI Prediction | Managed inference and model deployment | Hosted on GCP | Tight integration with Google ecosystem | Production ML workloads |

| Azure AI (Managed Inference) | Managed inference for Azure | Hosted on Azure | Enterprise integrations, Azure security | Enterprise AI deployments |

| CoreWeave Inference Platform | GPU-optimized bare-metal inference | Hosted / Cloud | High throughput, performance tuning | High-performance inference |

| Run:AI | GPU orchestration + inference scheduling | Self-managed / Cloud | Efficient resource utilization, scheduling | Inference at scale on shared GPU clusters |

| Hugging Face Inference API | Managed inference for open models | Hosted | Model marketplace, ease of use | Developers & startups |

| Paperspace / Gradient Inference | GPU inferencing & deployment tooling | Hosted / Cloud | Developer-friendly | ML apps, custom models |

| KServe (Kubeflow) | Open-source inference orchestration | Self-managed | Kubernetes native, extensible | Large-scale cloud native inference |

| Ray Serve (Ray) | Distributed model serving | Self-managed / Cloud | Flexible actor & batching models | Custom distributed inference |

| TorchServe (PyTorch) | PyTorch model server | Self-managed | Simple PyTorch deployment | PyTorch model deployments |

Main Investors

| Investor | Ownership % |

|---|---|

| Nvidia | ~0.5% |

| Accel | Undisclosed |

| Others (via $700M private placement Dec‑2024) | Undisclosed |

Founding History

- 1989: Founded as Yandex N.V. by Arkady Volozh as a internet search company ( Google of Russia ).

- 2022–24: Sanctions led to divestment of Russian assets (~$5.4B sale in July 2024), forming Nebius Group with retained non-Russia businesses.

- Oct 2024: Relaunched and re-listed on Nasdaq under ticker NBIS.

Before 2024 — Yandex Era

- Yandex N.V. existed since the 1990s as the Dutch parent of the Russian internet giant Yandex.

- Prior to 2024, Yandex’s focus was not on GPU cloud or AI-infrastructure services in the same way; it operated consumer internet products.

2023–2024 — Strategic Pivot

- Feb–Jul 2024: Russia’s invasion of Ukraine and ensuing sanctions led Yandex to divest its Russian business and retain international assets, refocusing on infrastructure and technology.

- July 2024: Yandex’s non-Russian assets were sold and reorganized as Nebius Group, a standalone AI infrastructure company. This marked the beginning of Nebius’s explicit transition toward GPU-centric cloud services for AI workloads.

Late 2024–2025 — GPU Cloud Buildout

- Late 2024: Nebius began aggressively building out large-scale GPU clusters and data centers in Europe and the U.S., positioning itself as a provider of AI-optimized cloud infrastructure (GPU training and inference) rather than traditional general-purpose cloud.

- 2025: Nebius publicly marketed Nebius AI Cloud and expanded GPU capacity with modern NVIDIA hardware (like H200/Blackwell), actively offering scalable GPU cloud services to developers and enterprise customers.