The Company

SanDisk is a leading provider of NAND flash memory storage solutions, supplying chips and storage products used in data centers, smartphones, PCs, automotive systems, and consumer devices. The company operates across both component (NAND chips) and end-product storage (SSDs, cards, USB) markets, making it a vertically integrated storage player.

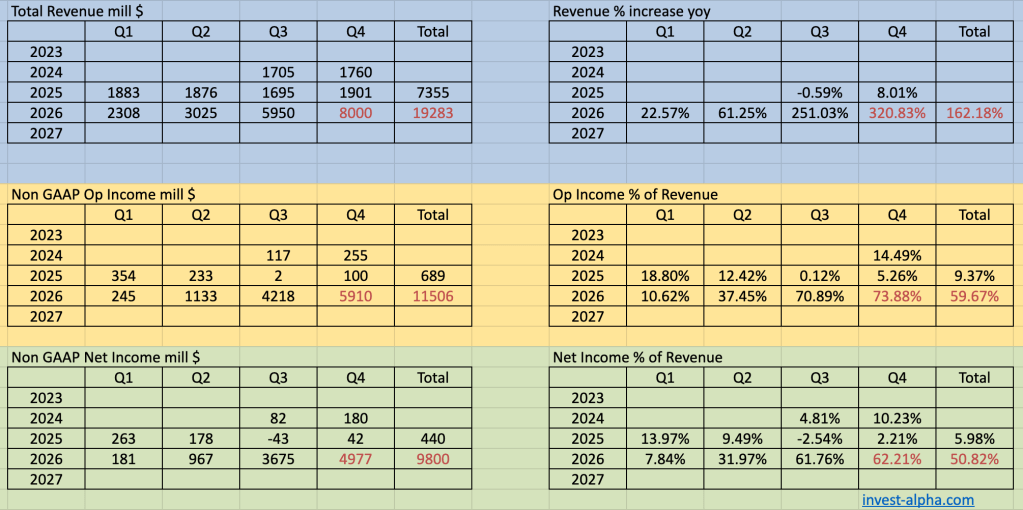

Financials

Bull Case for SNDK

- NAND cycle recovery → ASP expansion drives massive earnings leverage

- AI storage demand → inference + training require high-performance SSDs

- Mix shift toward enterprise SSDs (higher margin)

- Industry consolidation → improved pricing discipline

- Bit demand structurally growing faster than supply

Bear Case for SNDK

- NAND remains a commodity → pricing crashes recur

- Oversupply risk from competitors (Samsung, SK hynix)

- High capex → weak FCF in downturns

- Limited differentiation vs competitors

- AI upside may skew more toward compute (GPUs) than storage

Management Outlook

- Expect NAND recovery underway after deep downturn

- Focus on:

- Reducing supply growth (capex discipline)

- Driving higher-margin enterprise SSD mix

- Near-term:

- Gradual pricing recovery

- Margin improvement lagging pricing

- Long-term:

- AI + hyperscaler demand seen as structural tailwind

TAM & CAGR – NAND Flash & Storage Market

- Global NAND Flash TAM: ~$80B–$100B

- Projected CAGR (next 5 years): ~12–18%

Growth Drivers:

- AI data center storage demand (training + inference)

- Hyperscaler SSD adoption

- Smartphone storage density growth

- Automotive storage (ADAS, edge AI)

- PC refresh cycles (higher storage per device)

Products (Detailed Revenue Breakdown)

| Category | Products | Use Case | Approx % Revenue | Key Competitors |

|---|---|---|---|---|

| Client SSDs | NVMe SSDs (WD Black, Blue) | PCs, laptops | ~25–30% | Samsung, Micron |

| Data Center SSDs | Enterprise NVMe SSDs | Hyperscalers, AI storage | ~20–25% | Samsung, SK hynix |

| Mobile & Embedded NAND | UFS, eMMC | Smartphones, tablets | ~20–25% | Micron, Kioxia |

| Removable Storage | SD cards, microSD | Cameras, mobile | ~10–15% | Samsung, Kingston |

| USB & External Storage | USB drives, portable SSDs | Consumers, creators | ~10–15% | Seagate, Samsung |

| NAND Components (OEM) | Raw NAND wafers/dies | OEM integrations | ~10–15% | Micron, SK hynix |

Key Trend:

Shift from low-margin removable storage → high-value enterprise SSDs.

Business Model

- Vertically integrated NAND manufacturer

- Revenue streams:

- NAND component sales (commodity exposure)

- Branded storage products (higher margin)

- Long-term supply agreements with OEMs & hyperscalers

- Capital intensive → requires continuous node shrink investment

Economic Model:

- Revenue = (Bits shipped × ASP per bit)

- Profit = Highly sensitive to NAND pricing cycles

Customers

- Hyperscalers (cloud + AI workloads)

- Smartphone OEMs

- PC OEMs (Dell, HP, Lenovo)

- Automotive suppliers (ADAS storage)

- Consumers (retail storage products)

Top 3 Competitors (Direct Product Competition)

1. Samsung Electronics

- Market leader in NAND

- Strongest in enterprise SSD + vertical integration

2. Micron Technology

- Competes in NAND + DRAM

- Strong presence in data center SSD + mobile

3. SK hynix

- Growing NAND share (via Solidigm acquisition)

- Strong in enterprise SSDs for hyperscalers

Founding History

- Founded in 1988 by Eli Harari, Sanjay Mehrotra, and Jack Yuan

- Pioneer of flash memory storage technology

- Acquired by Western Digital in 2016

- Recently repositioned / separated to focus on pure-play NAND & flash storage