Lumentum (LITE) Company Overview

Lumentum Holdings designs and manufactures photonic products including lasers, optical components, and subsystems used in cloud data centers, telecom networks, and industrial applications. The company is a key supplier of optical technologies that enable high-speed data transmission and precision sensing.

Lumentum Financials Overview

- Revenue Profile: Cyclical, tied to cloud capex, telecom spend, and customer inventory digestion

- Gross Margins: Mid-to-high 30% range, expanding during cloud upcycles

- Operating Leverage: High — margins expand rapidly with volume recovery

- Balance Sheet: Net cash / low leverage, enabling cycle endurance

Key Dynamic: Lumentum’s financial performance is highly sensitive to cloud optical demand cycles, especially from hyperscale data centers transitioning to higher-speed interconnects.

Lumentum Bull Case

- AI-Driven Optical Upgrade Cycle

AI data centers require faster, denser optical interconnects (400G → 800G → 1.6T), directly benefiting Lumentum’s coherent optics and laser portfolio. - Strategic Exposure to Cloud Capex Recovery

As hyperscalers resume network upgrades after digestion phases, Lumentum sees sharp volume rebounds due to high fixed-cost leverage. - Technology Depth in Lasers & Modulation

Strong IP in tunable lasers, modulators, and integrated photonics creates switching costs for customers. - Operating Margin Upside

Incremental revenue carries outsized margin expansion, making earnings recovery nonlinear in upcycles.

Lumentum Bear Case

- Customer Concentration Risk

A small number of large cloud and telecom customers drive a significant portion of revenue. - Optical Component Pricing Pressure

Competition and vertical integration by hyperscalers could compress margins over time. - Capex Timing Uncertainty

Cloud optical demand comes in waves; prolonged digestion cycles can depress revenue for multiple quarters. - Technological Displacement Risk

Alternative optical architectures or in-house silicon photonics could reduce third-party component demand.

Lumentum Management Outlook Based on Most Recent Earnings

- Management has emphasized early signs of stabilization following customer inventory corrections.

- AI-related optical demand is expected to outgrow traditional telecom demand over the next cycle.

- Focus remains on:

- Cost discipline during downcycles

- Prioritizing high-margin cloud and datacom products

- Selective investment in next-gen coherent and laser platforms

Tone: Cautiously optimistic, with confidence in AI-driven multi-year demand but near-term visibility still limited.

Lumentum TAM and Market CAGR Outlook

- Total Addressable Market (TAM): ~$25–30 billion

- Includes cloud datacom optics, telecom optical components, and industrial photonics

- Expected CAGR (Next 5 Years): ~8–12%

- Cloud & AI optical networking: low-to-mid teens CAGR

- Telecom optics: mid-single digit CAGR

Structural Driver: Exploding east-west traffic inside AI data centers requiring higher-speed optical links.

Lumentum Management Outlook

- We previously identified three primary catalysts for Lumentum’s future growth: cloud transceivers, optical circuit switches (OCS), and co-packaged optics (CPO). The headline for this quarter is that the vast majority of this growth is still ahead of us, and we have increased confidence as to the timing and magnitude of the ramps.we are only just beginning to unlock the massive potential of OCS and CPO.

Lumentum Products and Revenue Mix

| Product Category | Sub-Category | Description | AI Relevance | % of Revenue (Approx) | Growth Profile |

|---|---|---|---|---|---|

| Optical transceivers Datacom | 100G / 400G / 800G / 1.6T optics | Used inside data centers for short distances of meters | Critical (core AI interconnect) | ~25–35% | High growth (15–25% CAGR) |

| Optical transceivers Telecom (Coherent) | Long-haul, metro DWDM | High-speed transmission across telecom networks over 100s of kilometers | Moderate | ~30–40% | Low growth / cyclical |

| Optical Components | Lasers, modulators, photodiodes | Core building blocks for transceivers and modules | High (enabler) | ~15–20% | Mid growth |

| Optical Circuit Switches (OCS) | MEMS-based switching | Dynamically routes optical signals between racks | Emerging AI architecture play | <5% (early) | Very high growth (early-stage) |

| Co-Packaged Optics (CPO) | Optics integrated with switch ASICs | Reduces power & latency vs pluggables | Next-gen AI infra | ~0–2% (R&D / pilot) | Explosive (post-2026) |

| 3D Sensing Lasers | VCSEL arrays | FaceID / consumer sensing | Low | ~10–15% | Cyclical |

| Industrial Lasers | Fiber lasers | Manufacturing, LiDAR | Low | ~5% | Stable |

Product Details

1. Cloud Transceivers (Near-Term Revenue Driver)

- This is where AI demand is already hitting

- Driven by:

- NVIDIA clusters

- Hyperscaler capex

- Transition path:

- 400G → 800G → 1.6T

This is the primary revenue growth engine today

2. Optical Circuit Switches (OCS) (Architecture Shift)

- Allows dynamic GPU-to-GPU connectivity

- Replaces:

- Static electrical switching layers

- Benefits:

- Lower latency

- Better utilization of expensive GPUs

This is a structural shift in AI cluster design

Key insight:

OCS becomes more valuable as:

- Cluster sizes scale (10K+ GPUs)

- East-west traffic explodes

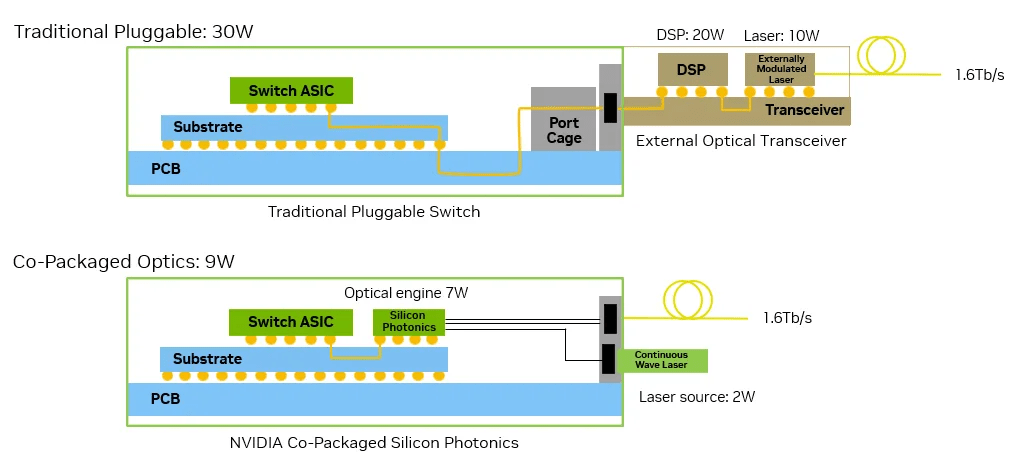

3. Co-Packaged Optics (CPO) (Next Wave Disruption)

- Moves optics inside the switch (next to ASIC)

- Solves:

- Power bottlenecks

- Signal integrity limits of pluggables

This is a post-800G paradigm shift

Timeline reality:

- 2025–2026 → Early deployments

- 2027+ → Meaningful adoption

How This Maps to Revenue Today vs Future

Today (2025–2026):

- Dominated by:

- Transceivers

- Telecom optics

- OCS + CPO = negligible revenue

Future (2027+):

- Mix shifts toward:

- Transceivers (still large)

- OCS (meaningful)

- CPO (potentially disruptive)

Lumentum Customers

- Hyperscale Cloud Providers (via OEMs)

- Optical Networking Equipment Vendors

- Telecom Carriers

- Industrial Equipment Manufacturers

End markets span AI data centers, backbone networks, and precision manufacturing.

Lumentum Competitors

- Coherent

Broad photonics portfolio with overlap in lasers and optical components. - Broadcom

Competes indirectly via optical interconnect and silicon photonics solutions.

| Product Area | Lumentum Position | Key Competitors | Who’s Leading Today | Key Notes |

|---|---|---|---|---|

| Optical transceivers Datacom (400G / 800G / 1.6T) | Strong but not dominant | Coherent (COHR), Applied Optoelectronics (AAOI), Innolight, Eoptolink | Innolight / AAOI (cost & scale) | LITE gaining share but pricing pressure intense |

| Optical transceivers Telecom (DWDM / Long-haul) | Strong (post NeoPhotonics) | Coherent (COHR), Ciena, Nokia | LITE / COHR | Mature, lower growth, still large revenue base |

| Optical Components (lasers, modulators) | Strong | Coherent (COHR), II-VI legacy, Broadcom | Fragmented leadership | Vertical integration matters |

| Optical Circuit Switches (OCS) | Early leader | Coherent (COHR), startups | LITE (early positioning) | Still nascent but strategic for AI clusters |

| Co-Packaged Optics (CPO) | Participating / early | Broadcom (AVGO), Nvidia ecosystem, Marvell (MRVL) | Broadcom leading | Hyperscaler + switch ASIC integration advantage |

| Active Electrical Cables (AEC) (Substitute tech) | No presence | Credo (CRDO), Astera Labs (ALAB) | CRDO / ALAB | Major competitive threat to optics |

| 3D Sensing (VCSEL lasers) | Strong | Coherent (COHR), AMS-OSRAM | LITE historically strong | Apple exposure, volatile |

| Industrial Lasers | Moderate | Coherent (COHR), IPG Photonics | COHR / IPG | Not a core growth driver |

Lumentum Founding History

Lumentum was spun out of JDS Uniphase in 2015, inheriting decades of optical networking expertise. Since then, the company has focused on higher-growth, higher-margin photonics markets, pivoting toward cloud data centers and advanced optical components.